Data maps help consumers get a better deal on health insurance for 2018’s Open Enrollment

Editor’s note: The following is a guest post by Ashley Semanskee, a Research Assistant at the Kaiser Family Foundation’s Program for the Study of Health Reform and Private Insurance.

Right now, we’re in the midst of Open Enrollment, the six-week period from November 1– December 15, when consumers can sign up for 2018 plans on healthcare.gov. While buying health insurance is a major financial decision for everyone, choosing the best plan for yourself, your family and your financial situation may seem more complicated than ever. And for consumers getting their health insurance through the individual market, shopping for 2018 coverage is more confusing due to the shortened enrollment period, reduced funding for Navigators (enrollment assistance programs), and renewal notices causing misleading sticker shock.

Despite headlines about skyrocketing rates, we’ve seen peculiar dynamic effect 2018 premiums: while premiums for unsubsidized consumers are rising on average, consumers eligible for tax credits may actually pay less than last year.

Shopping for health insurance is confusing: premiums are rising for some and falling for others

Typically, consumers shopping in the individual market choose from four tiers of health coverage: bronze, silver, gold, and platinum. Bronze plans have the lowest monthly premiums, but the highest deductibles and copays. Gold and platinum plans offer more financial protection if you get sick, but typically have the highest monthly premiums. Silver plans are the most popular level of coverage because they fall in between the two extremes. This year, many people are eligible for tax credits that cover part of their premium; the tax credit amount is pegged to the cost of silver plans. Low-income people also qualify for cost-sharing reductions; insurers are required to offer them lower deductibles and copays.

In October, the Trump Administration ceased payments to insurers for cost-sharing reductions (CSRs). Insurers are still required by law to offer reduced deductibles and copays to their low-income customers, but they will no longer be reimbursed by the federal government for doing so. To offset the cost of lost CSR payments, most insurers raised premiums. However, the strategy that insurers used to offset these costs has important implications for what people will actually pay.

Most insurers loaded the cost of CSR payments entirely onto premiums for silver plans. Since the amount of premium tax credit rises dollar for dollar with silver plans, this means that subsidized consumers will pay about the same as last year for silver plans, and could pay much less for bronze or gold plans. For some people, their increased tax credit will cover the entire premium for a bronze plan. For others, a gold plan will actually have a lower or comparable premium to a silver plan (as well as a smaller deductible). Consumers will have to determine if any of these scenarios apply to them, and weigh lower premiums on some plans against higher cost sharing. If this sounds complicated, you are not alone in your confusion.

Interactive data maps help consumers and reporters make sense of it all

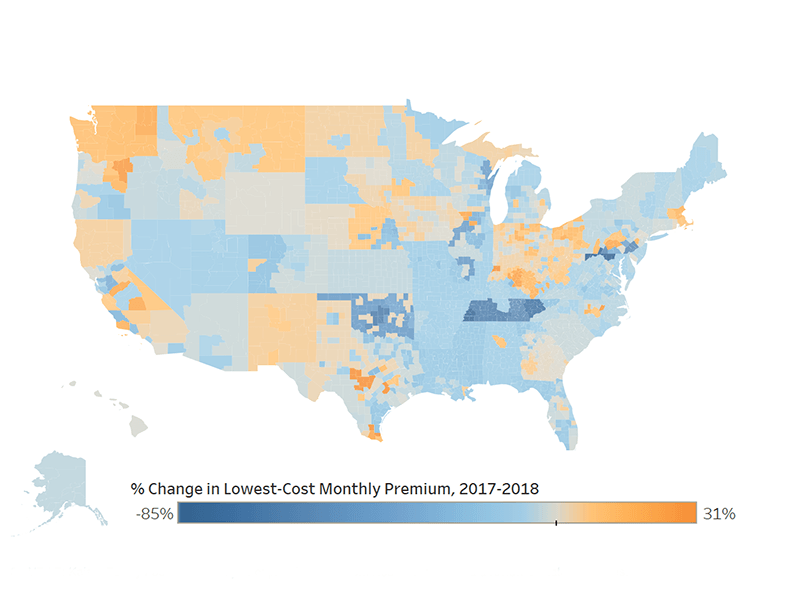

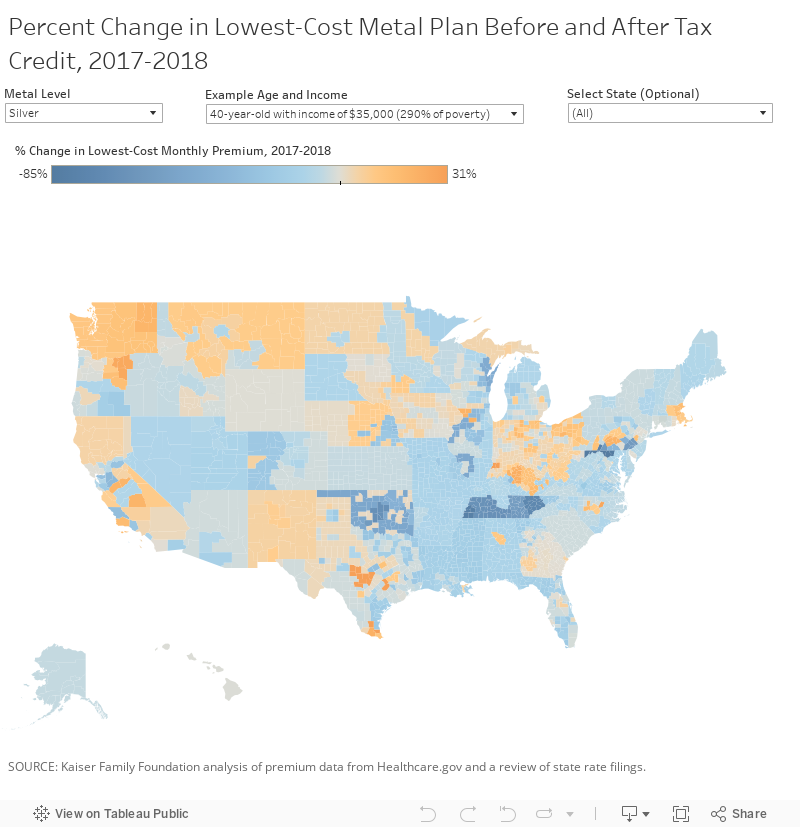

To help people understand how premiums are changing in 2018, the Kaiser Family Foundation (KFF) used Tableau Public to build an interactive, county-level map. The map allows people to select a metal level (bronze, silver, or gold) and an example income from a dropdown parameter. Interacting with the map allows people to see the data story for themselves: while premiums are rising in much of the country for unsubsidized people, net premiums are decreasing on average for those with subsidies, especially for bronze and gold plans.

People can visualize the larger trends and pull specific examples for their own county in the rollover tooltip; they can even filter the map to a specific state of interest. This map also helps reporters find the extreme examples, and investigate why some areas of the country are experiencing steep premium increases.

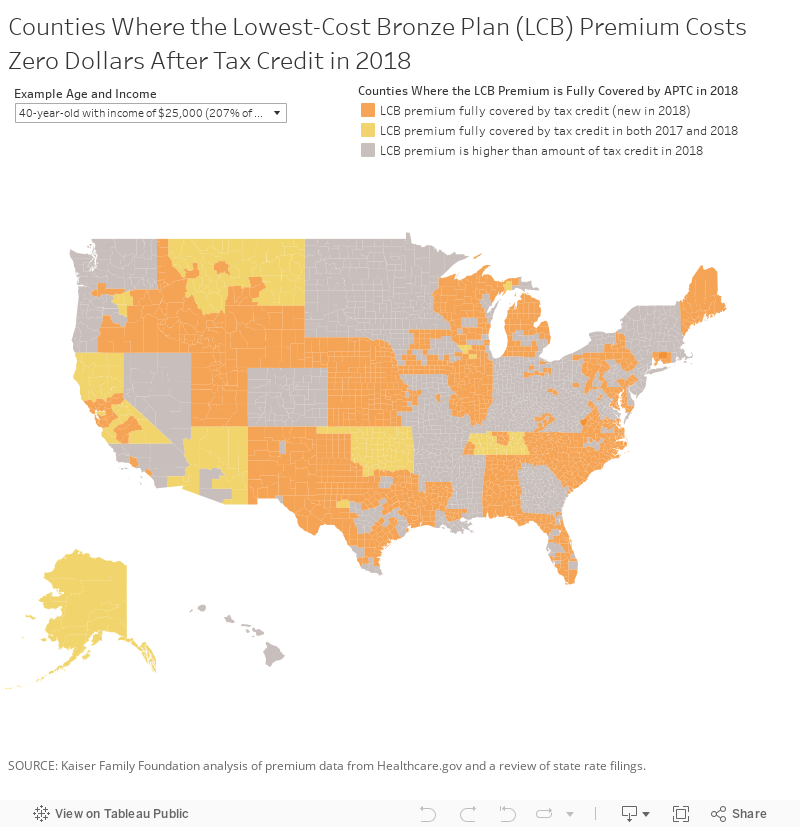

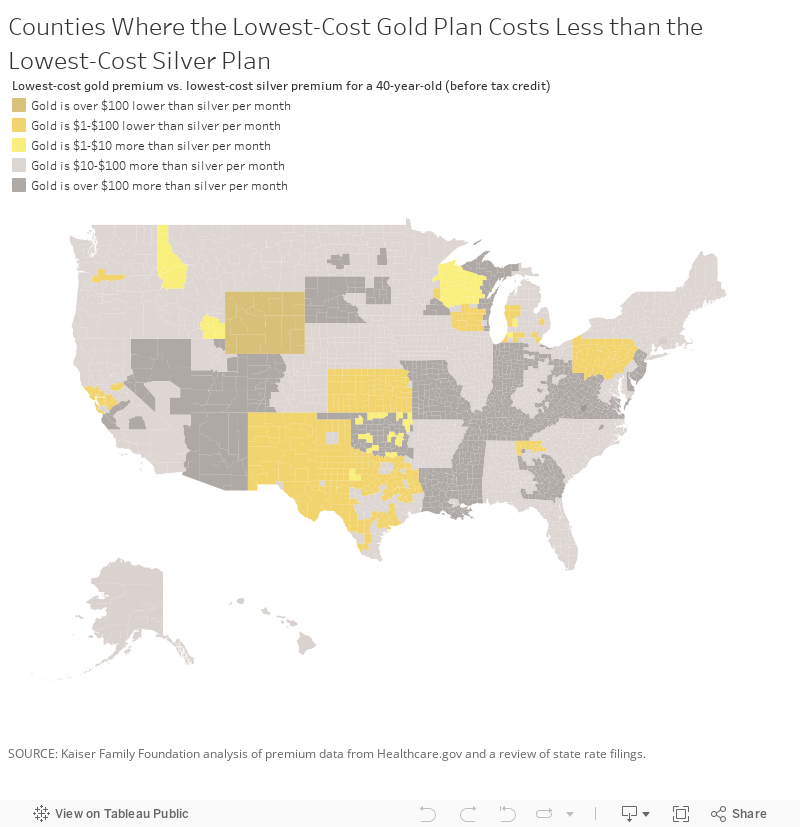

KFF has also published two additional maps that show where people may be better off switching to bronze or gold plans:

This map shows where subsidized people can purchase a bronze plan for no additional premium. KFF estimates at least 4.5 million currently uninsured people could obtain a bronze plan at no cost in 2018, after taking their premium tax credit into account. In this map, the orange and yellow counties indicate where an individual’s tax credit would cover the full cost of the cheapest bronze plan in their area.

Additionally, this map shows where consumers could be better off switching from a silver plan to a gold plan. The yellow and gold counties are where the least expensive gold plans for a 40-year-old cost less than the lowest-cost silver plan (before subsidies). Consumers in these counties could be better off switching to gold, because they would pay less per month and have lower deductible and copays.

It is important to note that these maps only show estimated premiums for a 40-year-old at example income levels. What you will actually pay for health insurance depends on your family situation—where you live, how much money you make, your age, and the size of your household. Nevertheless, these maps can help consumers and reporters make sense of the counterintuitive way premiums are changing this year.

Results so far

There is some indication that consumers are taking advantage of higher tax credits in 2018. Data from Health Sherpa, an online health insurance broker, shows that a third of their customers purchased plans for less than $10 a month, and 18% of their customers enrolled in a plan with $0 monthly premium. Covered California data shows that more consumers are using their increased tax credits to purchase more comprehensive coverage, with 3x as many enrollees choosing gold plans compared to last year. As Open Enrollment continues, it is more important than ever for everyone to shop around, and carefully consider their options—and try using a data visualization to help them make the best decision. To see more data visualizations from the Kaiser Family Foundation, check out our Tableau Public Profile here.

Related Stories

Using data to drive conversations about climate change

April 28, 2022

April 28, 2022

Leveraging data to improve forestry practices worldwide

Doing Good Data Means Doing No Harm

December 13, 2021

December 13, 2021

Subscribe to our blog

Get the latest Tableau updates in your inbox.